- Earlier this week, Li Auto joined the Brussels-based China Chamber of Commerce to the EU as a full member, deepening its European expansion through an R&D center in Munich, new overseas retail locations, and hiring local sales leaders to build a compliant, localized operation.

- This move signals Li Auto’s push to shift from reliance on parallel exports toward direct engagement with EU regulators and premium competitors, potentially reshaping its role in the global EV landscape.

- We’ll now examine how Li Auto’s deeper integration into European institutions could affect its previously Europe-focused long-term investment narrative.

The latest GPUs need a type of rare earth metal called Neodymium and there are only 31 companies in the world exploring or producing it. Find the list for free.

Li Auto Investment Narrative Recap

To own Li Auto, you need to believe it can transition from China centric EREV reliance to a profitable BEV and software led model while funding heavy R&D and capex. Right now, the key near term catalyst is how upcoming earnings shape confidence in that transition, while liquidity pressure and rising competition remain the biggest risks. The new EU chamber membership does not materially change those immediate drivers, but it sharpens the focus on execution overseas.

Among recent developments, China’s new export license requirement for EV makers starting January 1, 2026 directly intersects with Li Auto’s push into Europe. As Li shifts from parallel exports to more direct, compliant operations in the EU, investors may watch how license based constraints interact with its Munich R&D work and overseas retail rollout, and whether those efforts offset or compound the regulatory and timing risks embedded in its international expansion catalyst.

Yet even with Li Auto’s push into Europe, investors should be aware of how new export licensing rules could…

Read the full narrative on Li Auto (it’s free!)

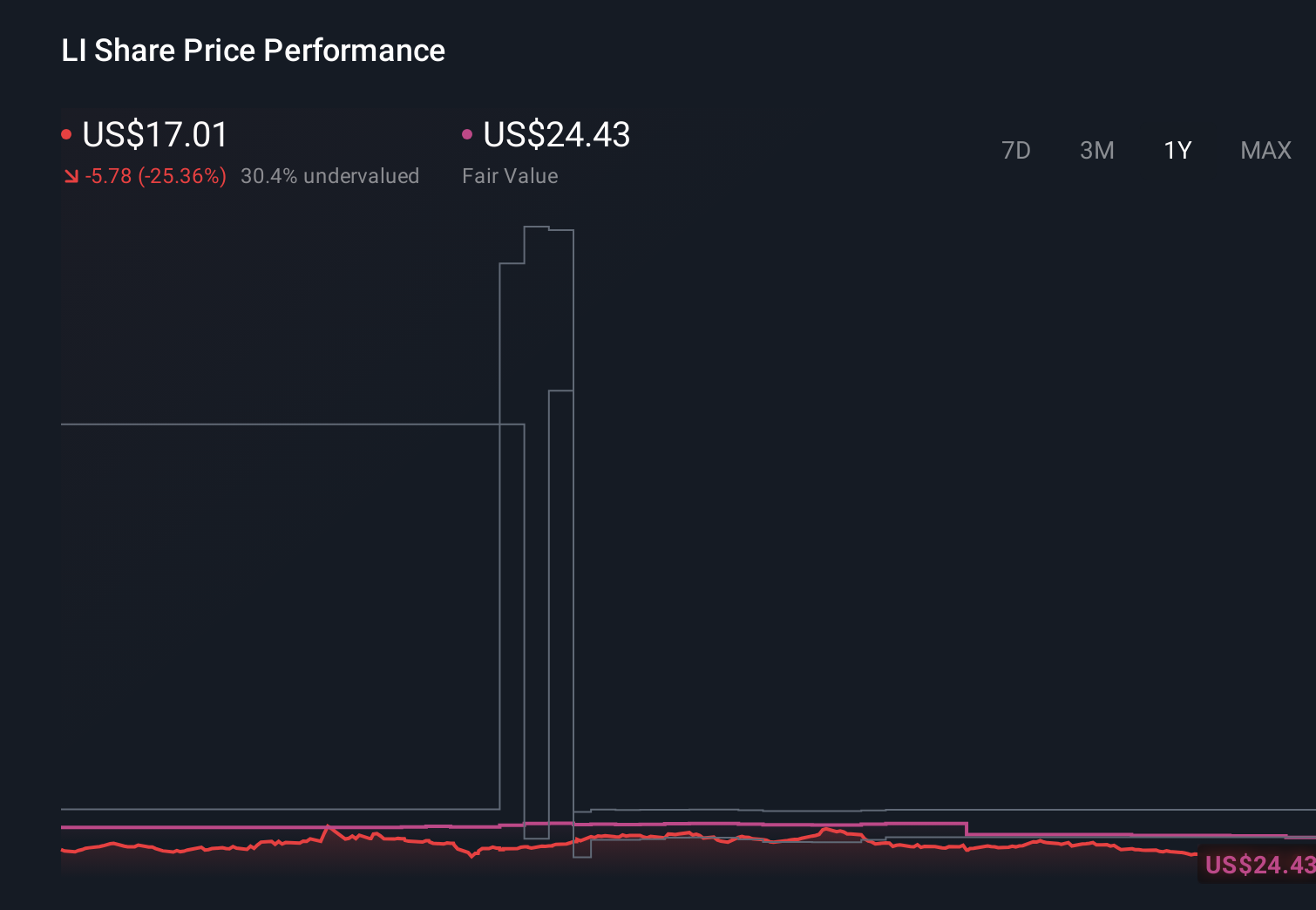

Li Auto’s narrative projects CN¥232.1 billion revenue and CN¥15.2 billion earnings by 2028.

Uncover how Li Auto’s forecasts yield a $24.43 fair value, a 36% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming revenue could reach about CN¥372,500,000,000 by 2028, yet this new EU focused development may either reinforce or challenge that overseas expansion narrative, so it is worth comparing those bullish views with the risk that geopolitical and regulatory frictions could still constrain Li Auto’s room to grow.

Explore 6 other fair value estimates on Li Auto – why the stock might be worth just $22.18!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don’t miss this chance:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}