Europe Sustainable Fashion Market Summary

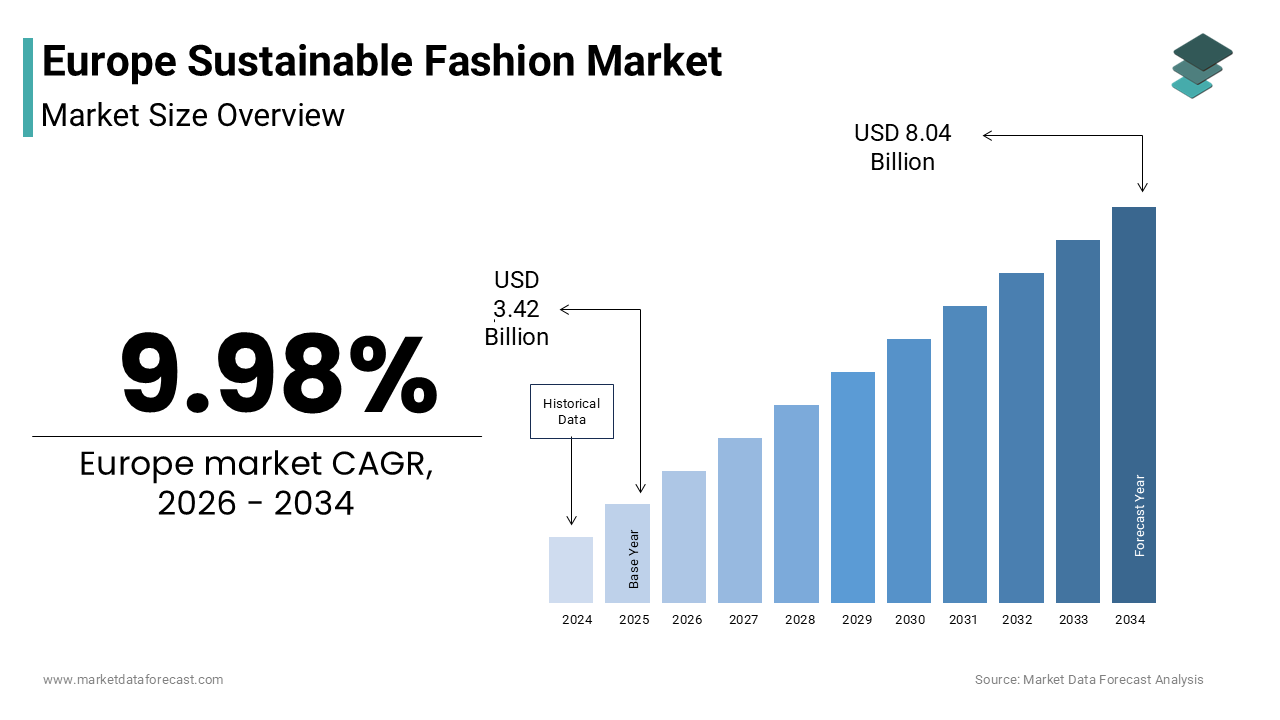

The Europe sustainable fashion market was valued at USD 3.42 billion in 2025 and is expected to reach USD 8.04 billion by 2034, growing at a CAGR of 9.98% during the forecast period. Market growth is driven by increasing consumer awareness of environmental and ethical issues, stringent EU regulations promoting circular economy practices, and rising demand for eco-friendly and transparent fashion products. The shift from fast fashion to sustainable and circular models, along with advancements in bio-based materials and resale platforms, is accelerating market expansion across Europe.

Key Market Trends

- Rising demand for ethical and sustainable clothing is driven by conscious consumer behavior, especially among Millennials and Gen Z

- Rapid adoption of circular fashion models including resale, rental, and repair services

- Strong regulatory push from the EU promoting durability, recyclability, and digital product transparency

- Increasing innovation in bio-based, regenerative, and recycled materials

- The growing importance of supply chain transparency and certification standards to build consumer trust

Segmental Insights

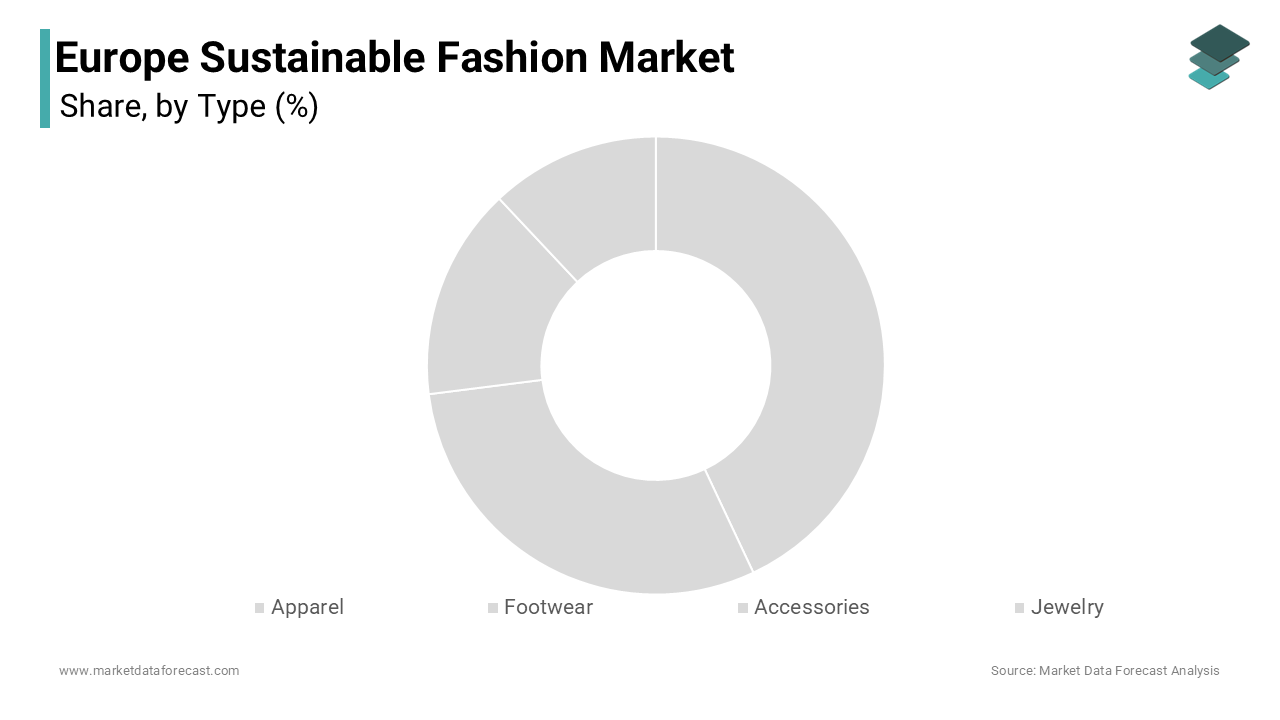

- By Type, the Apparel segment dominates with 64.1% share due to high consumption volume and regulatory focus on textile waste

- By Material, the Organic/natural materials lead with 52.8% share, driven by consumer preference for biodegradable and non-toxic fabrics.

- By End User, the women segment holds the largest share (58.3%) due to higher purchase frequency and strong alignment with sustainability values

Regional Insights

- Germany leads the market with a 22.8% share, supported by strong environmental awareness and advanced recycling infrastructure

- United Kingdom shows strong growth driven by resale culture, activism, and ethical fashion adoption.

- France focuses on sustainable luxury and strict anti-waste regulations

- Italy leverages textile innovation and heritage craftsmanship for sustainable production

- Sweden emerges as a key innovation hub with strong circular economy initiatives and conscious consumer behavior

Competitive Landscape

The market is highly competitive, with fast fashion giants, luxury brands, and emerging sustainable labels competing through innovation, transparency, and circular strategies. Companies are increasingly investing in recycling technologies, bio-based materials, and digital product passports to meet regulatory requirements and consumer expectations. Key players include Stella McCartney, Patagonia, H&M Group, Inditex (Zara), Adidas AG, Puma SE, Nike Inc., Levi Strauss & Co., Burberry, Kering SA, Eileen Fisher, People Tree, Reformation, Armedangels, and Pangaia.

Europe Sustainable Fashion Market Size

The Europe sustainable fashion market size was valued at USD 3.42 billion in 2025 and is anticipated to reach USD 3.76 billion in 2026 from USD 8.04 billion by 2034, growing at a CAGR of 9.98% during the forecast period from 2026 to 2034.

Sustainable fashion is an ethical and eco-conscious approach to designing, producing, and consuming clothing that minimizes environmental impact, promotes fair labor practices, and prioritizes durability over disposable trends. This paradigm shifts away from the linear take-make-dispose model toward a circular economy emphasizing durability, recyclability, and ethical labor practices. The definition encompasses garments made from organic or recycled fibers, produced with reduced water and energy consumption, and distributed through transparent channels that verify fair wages. The urgency for this transition is underscored by the severe ecological footprint of traditional fashion. According to the European Environment Agency, the textile industry is the fourth largest contributor to environmental pressure in Europe, utilizing vast quantities of water and generating significant greenhouse gas emissions. Furthermore, Eurostat and regional environmental briefings indicate that the amount of textiles discarded by the average European consumer has reached record highs, yet the vast majority of these materials are incinerated or landfilled rather than being recycled back into new garments. The European Commission has responded by launching the Strategy for Sustainable and Circular Textiles, aiming to make all textile products on the EU market durable, repairable, and recyclable by 2030. This regulatory push, combined with rising consumer consciousness regarding climate change, redefines the market not merely as a commercial segment but as a critical component of the continent’s Green Deal objectives. The market thus operates at the intersection of regulatory compliance, technological innovation, and evolving cultural values regarding consumption.

MARKET DRIVERS

Intensified Consumer Awareness and Ethical Purchasing Behavior

Shift Toward Conscious Consumption Patterns

A profound shift in consumer consciousness contributes to the growth of the Europe sustainable fashion market. Purchasing decisions are now increasingly dictated by ethical considerations and environmental impact rather than price alone. Modern European consumers, particularly Millennials and Generation Z, possess a heightened awareness of the social and ecological costs associated with fast fashion, driving demand for transparency and responsibility. According to a study, 67 percent of European consumers consider the use of sustainable materials to be an important purchasing factor, while 63 percent actively seek out brands that demonstrate clear commitments to reducing their carbon footprint. This sentiment is further amplified by the rise of digital activism, where social media platforms serve as conduits for exposing labor abuses and environmental degradation, forcing brands to adapt or face reputational ruin. Research from the European Consumer Organisation indicates that most EU shoppers are prepared to pay a modest price increase for products that carry ethical or sustainable certifications. Furthermore, the proliferation of certification labels such as GOTS and Fair Trade has empowered consumers to make informed choices, creating a market dynamic where sustainability acts as a key differentiator. Research suggest that younger generations increasingly view their purchasing power as a form of social and political expression, making transparent sustainability efforts essential for brand relevance. This behavioral evolution ensures that ethical credentials are no longer optional but essential for market survival and growth.

Robust Regulatory Frameworks and Circular Economy Mandates

Legislative Pressure Driving Industry Transformation

The European Union is implementing stringent regulatory frameworks and circular economy mandates, which boost the expansion of the Europe sustainable fashion market. These policies compel industry players to adopt sustainable practices or face significant penalties. The EU is globally recognized as a pioneer in environmental legislation, and its recent initiatives are reshaping the operational landscape for fashion brands operating within its borders. The European Commission’s textile strategy now requires manufacturers to move away from “fast fashion” models by ensuring products are built for durability and are easy to repair or recycle. Under the Ecodesign for Sustainable Products Regulation, new textile goods will be required to feature digital passports, providing full transparency regarding material origins and environmental footprints to eliminate supply chain opacity. Furthermore, the proposed Extended Producer Responsibility schemes will hold manufacturers financially accountable for the end-of-life management of their products, incentivizing the design of circular systems. The European Parliament is championing comprehensive measures to drastically lower the volume of textiles sent to landfills or incinerators, focusing on high-volume recycling and stricter waste management protocols for the end of the decade. Additionally, through the Corporate Sustainability Reporting Directive, large enterprises are now legally obligated to provide detailed public disclosures regarding their social and environmental impact, fostering higher levels of corporate transparency. The Ellen MacArthur Foundation suggests that upcoming regulatory deadlines are forcing a surge in private investment toward advanced recycling technologies and the development of next-generation sustainable materials. This legislative backbone provides a stable and enforceable foundation for market growth, ensuring that sustainability becomes embedded in the core business strategies of all major players.

MARKET RESTRAINTS

High Production Costs and Premium Pricing Barriers

Economic Constraints Limiting Mass Adoption

The high cost of ethical materials and labor hampers the growth of the Europe sustainable fashion market. These factors lead to premium retail prices that alienate price-sensitive consumers. Producing garments using organic cotton, recycled fibers, or innovative bio-based materials often incurs costs that are higher than conventional methods due to limited supply chains, specialized processing requirements, and fair wage mandates. These increased input costs are inevitably passed down to the consumer, resulting in retail prices that are often inaccessible to the average household, particularly amidst the current cost of living crisis affecting many European nations. Research indicates that while a notable share of Europeans express a desire to buy sustainable fashion, only a portion actually follow through with purchases when faced with significantly higher price points. This “attitude-behavior gap” is exacerbated by inflation, which forces consumers to prioritize affordability over ethics. Furthermore, small and medium-sized enterprises often lack the capital reserves to absorb these initial costs or invest in the necessary certifications, limiting their ability to compete with larger conglomerates. As per sources, the financial burden of transitioning to sustainable practices remains a formidable barrier for independent designers and emerging brands, stifling innovation and diversity within the market. High pricing will continue to restrict the market to a niche, affluent demographic. This will last until economies of scale drive down costs or subsidies become more widely available.

Complex Supply Chain Transparency and Verification Issues

Operational Opacity Hindering Credibility

Inherent complexity and opacity of global fashion supply chains remain an impediment to the Europe sustainable fashion market. This makes verifying sustainability claims and ensuring end-to-end traceability exceptionally difficult and resource-intensive. The fashion industry relies on fragmented networks spanning multiple countries, involving numerous tiers of suppliers from raw material growers to spinners, weavers, dyers, and manufacturers, each adding a layer of complexity to tracking. According to a study, fewer number of fashion brands have full visibility into their Tier 2 and Tier 3 suppliers, where the most significant environmental and social risks often reside. This lack of transparency creates fertile ground for greenwashing, where companies make unsubstantiated or misleading claims about their sustainability efforts, eroding consumer trust and diluting the value of genuine initiatives. A study reveals that a notable share of sustainability claims made by European fashion brands are unsubstantiated or misleading, highlighting the severity of the verification challenge. Implementing robust tracking systems such as blockchain requires significant technological investment and collaboration across competitors, which many firms are reluctant to undertake. Furthermore, the absence of a unified global standard for defining “sustainable” leads to confusion and inconsistency, making it hard for consumers to distinguish between credible certifications and marketing fluff. The sustainable fashion market’s credibility is currently compromised. Until the industry establishes seamless, tamper-proof traceability, consumer confidence and market expansion will remain stalled.

MARKET OPPORTUNITIES

Advancement of Circular Business Models and Resale Platforms

Unlocking Value Through Reuse and Recycling

The rapid advancement of circular business models, particularly the resale, rental, and repair sectors, offers a major opportunity for the Europe sustainable fashion market. This creates a pathway to decouple growth from resource extraction. As consumers increasingly embrace the idea of accessing fashion without ownership, the secondhand market is experiencing exponential growth, offering a viable pathway to extend garment lifecycles and reduce waste. The surge is driven by both economic incentives, as consumers seek affordable alternatives to new clothing, and environmental consciousness, as buying used significantly lowers the carbon footprint of fashion consumption. Major luxury and high street brands are capitalizing on this trend by launching their own resale platforms or partnering with established players like Vinted and Vestiaire Collective, thereby retaining control over their brand image while tapping into the circular economy. Furthermore, the rise of clothing rental services for occasion wear and subscription boxes for everyday items is gaining traction, particularly among urban professionals who value variety over possession. Additionally, innovations in chemical recycling technologies are enabling the transformation of old textiles into new high-quality fibers, closing the loop and reducing reliance on virgin materials. Brands can unlock new revenue streams and build deeper customer loyalty by adopting circular strategies. Doing so also helps them lead the way in the sustainability transition.

Innovation in Bio-Based and Regenerative Materials

Technological Breakthroughs in Material Science

The development and commercialization of innovative bio-based and regenerative materials provide a strong potential to revolutionize the raw material base of the European sustainable fashion market. This approach moves beyond the limitations of conventional cotton and synthetic fibers. Scientists and startups across Europe are pioneering the creation of textiles derived from agricultural waste, algae, mycelium, and lab-grown cellulose, which offer superior environmental profiles including lower water usage, biodegradability, and carbon sequestration potential. According to research, investment in next-generation material startups in Europe has doubled in the last three years, signaling strong confidence in the scalability of these solutions. For instance, materials made from pineapple leaves or mushroom roots are already being adopted by luxury brands for leather alternatives, providing cruelty-free and low-impact options that do not compromise on quality or aesthetics. Furthermore, the shift toward regenerative agriculture, which focuses on soil health and biodiversity, presents an opportunity to source cotton and wool in ways that actively restore ecosystems rather than deplete them. A study indicates that regenerative farming practices can sequester significant amounts of carbon, turning fashion supply chains into carbon sinks. This material revolution not only addresses the environmental deficits of traditional textiles but also opens up new narratives for branding and consumer engagement centered on innovation and nature positivity.

MARKET CHALLENGES

Prevalence of Greenwashing and Erosion of Consumer Trust

Credibility Crisis in Sustainability Claims

Greenwashing is a major challenge for the European sustainable fashion market. In this market, companies often falsify their environmental credentials, a deceptive practice that heavily erodes consumer trust and breeds skepticism toward real sustainability initiatives. As the demand for eco-friendly products surges, many brands have rushed to capitalize on the trend by using vague terminology like “eco-conscious” or “green” without substantiating these claims with data or third-party certifications. According to a sources, a considerable share of green claims given by fashion companies in the EU were found to be vague, misleading, or unfounded, creating a confusing landscape for shoppers. This deception dilutes the efforts of truly sustainable brands and makes it increasingly difficult for consumers to differentiate between authentic leaders and opportunistic marketers. The resulting cynicism can lead to “sustainability fatigue,” where consumers disengage entirely from the cause, believing that no brand is truly making a difference. Research suggests that a share of European consumers now doubt the validity of sustainability claims made by fashion retailers, a figure that has risen sharply in recent years. Furthermore, the lack of standardized definitions and enforcement mechanisms allows bad actors to operate with impunity, undermining the integrity of the entire market. Restoring trust will require radical transparency, rigorous independent auditing, and a unified industry stance against deceptive practices, tasks that are complex and resource-intensive to implement.

Infrastructure Deficits in Textile Waste Management and Recycling

Logistical Bottlenecks in Circular Systems

Severe deficit in infrastructure for textile waste management is a serious constraint to the European sustainable fashion market. This lack of collection, sorting, and recycling facilities hampers the realization of a truly circular economy. Despite ambitious EU targets for waste reduction, the current physical and technological capacity to handle the volume of discarded textiles is grossly insufficient, leading to high rates of landfilling and incineration. The complexity of modern garments, which often blend natural and synthetic fibers, makes mechanical recycling difficult and economically unviable without advanced separation technologies that are not yet widely deployed. Furthermore, the lack of standardized collection systems across different member states creates fragmentation, making it difficult to aggregate sufficient volumes of waste to feed large-scale recycling plants. Without a robust network of collection points, automated sorting hubs, and industrial-scale recycling facilities, the vision of closing the loop on fashion remains theoretical. Bridging this infrastructure gap requires coordinated public-private partnerships and significant capital expenditure, posing a daunting logistical and financial hurdle for the industry.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

9.98% |

|

Segments Covered |

By Type , Material, End User, Distribution Channel and Region. |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Country Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

Stella McCartney, Patagonia, H&M Group, Inditex (Zara), Adidas AG, Puma SE, Nike Inc., Levi Strauss & Co., Burberry Group plc, Kering SA, Eileen Fisher, People Tree, Reformation, Armedangels, and Pangaia |

SEGMENTAL ANALYSIS

By Type Insights

The apparel segment dominated the Europe sustainable fashion market and accounted for a 64.1% share in 2025. This dominance of the segment is intrinsic to the nature of the industry, as clothing constitutes the largest volume of textile consumption and waste generation across the continent. The sheer frequency of purchase cycles for garments compared to footwear or accessories ensures that this category remains the primary focus for both consumers and regulatory bodies aiming to reduce environmental impact. The main reason the apparel segment leads the way is the immense volume of clothing consumed annually by European households, which creates a massive addressable market for sustainable alternatives. Despite growing awareness, the turnover rate for garments remains high, necessitating a urgent shift toward eco-friendly production methods to mitigate waste. According to sources, Europeans purchase significant kilograms of textiles per person each year, with clothing making up the bulk of this figure. This high consumption rate means that even a small percentage shift toward sustainable options results in significant market value. The prevalence of fast fashion has normalized frequent purchasing, but the backlash against this model is strongest within the apparel category where visibility of waste is highest. As consumers become more conscious of the carbon footprint associated with producing a single t-shirt or pair of jeans, they are actively seeking organic cotton, linen, and recycled blends for their daily wear. The scale of the problem drives the scale of the solution, forcing major retailers to prioritize sustainable lines in their core apparel collections to maintain market relevance and comply with impending EU regulations on textile waste. Moreover, a further factor fueling the apparel segment is the intense regulatory scrutiny directed specifically at clothing waste and the implementation of Extended Producer Responsibility schemes. Governments across Europe are targeting the apparel industry as the primary source of textile pollution, mandating that brands take responsibility for the entire lifecycle of their garments. These regulations compel brands to redesign their apparel lines to minimize waste and maximize recyclability, driving innovation and investment in this segment. The introduction of digital product passports will initially target apparel items to provide transparency on materials and origin, further cementing this segment’s centrality in the sustainability debate. Furthermore, national laws in countries like France and Germany already require separate collection of textile waste, with clothing comprising the vast majority of collected items. This legislative pressure ensures that the apparel sector receives the lion’s share of funding, research, and consumer attention, solidifying its position as the dominant force in the sustainable fashion market.

The footwear segment is likely to experience the fastest CAGR of 9.8% during the forecast period. This rapid acceleration of the segment is propelled by technological breakthroughs in bio-based materials, a surge in demand for ethical athletic wear, and the increasing complexity of recycling shoes which has sparked innovative circular business models. Sustainable footwear stays on top mainly because the revolutionary development and adoption of bio-based materials that replace traditional leather and petroleum-based synthetics. Consumers are increasingly rejecting animal leather due to ethical concerns and synthetic materials due to their plastic content, creating a vacuum that innovative startups and established brands are rushing to fill with alternatives derived from mushrooms, pineapples, grapes, and algae. According to research, investment in next-generation leather alternatives in Europe has tripled in the last three years, with several commercial-scale facilities now operational. Brands are launching sneakers made entirely from mycelium or corn waste, appealing to environmentally conscious buyers who do not want to compromise on style or performance. The ability to market shoes as completely plastic-free or biodegradable offers a powerful unique selling proposition that drives premium pricing and brand loyalty. Furthermore, advancements in processing technologies have improved the durability and water resistance of these novel materials, overcoming previous technical barriers. As these materials move from niche prototypes to mass production, the cost differential is narrowing, making sustainable footwear accessible to a broader demographic and fueling exponential market expansion. In addition, another major pillar supporting this segment dominance is the emergence of specialized circular business models designed to address the historical difficulty of recycling complex shoe structures. Unlike simple garments, shoes are composed of multiple glued materials that are hard to separate, but new take-back schemes and design-for-disassembly principles are turning this challenge into an opportunity. These initiatives resonate strongly with consumers who feel guilty about discarding durable goods, offering a clear path for responsible disposal. Data from Vinted and other resale platforms shows that the secondhand footwear market is growing faster than general apparel, driven by the durability of shoes and the rise of sneaker culture which values vintage and limited editions. The integration of modular design, where parts of the shoe can be easily replaced or upgraded, is also gaining traction among tech-savvy consumers. Brands are unlocking new revenue streams and deepening customer engagement by solving the end-of-life puzzle. As a result, footwear has become the most dynamic and rapidly evolving segment in the sustainable fashion landscape.

By Material Insights

The Organic/Natural Materials segment led the Europe sustainable fashion market and captured a 52.8% share in 2025. This leading position of the segment is attributed to the long-standing consumer familiarity with natural fibers like organic cotton, linen, hemp, and wool, which are perceived as inherently safer, healthier, and more biodegradable than synthetic alternatives. The key strength keeping this segment in the lead is the strong consumer perception that these fibers are healthier for the skin and the environment due to their biodegradable nature and absence of toxic chemicals. European shoppers are increasingly wary of microplastic shedding from synthetic fabrics and the pesticide residue found in conventional cotton, leading them to prefer certified organic options. The knowledge that natural fibers decompose completely at the end of their life cycle, unlike polyester which persists for centuries, acts as a powerful psychological driver for purchase decisions. Furthermore, the tactile quality and breathability of natural fibers like linen and hemp are highly valued in the European climate, reinforcing their popularity beyond just ethical considerations. The established supply chains for organic cotton and wool, supported by decades of certification infrastructure like GOTS, make these materials readily available to brands, facilitating their widespread adoption. As awareness of the health impacts of microplastics grows, the preference for natural, breathable, and earth-returning materials will continue to underpin this segment’s market dominance. Furthermore, a key driver for apparel sector leadership is the maturity of their supply chains and the widespread recognition of robust certification standards that verify their sustainability claims. Unlike newer innovative materials that often lack standardized verification, organic cotton, linen, and wool benefit from well-established frameworks such as the Global Organic Textile Standard and the Responsible Wool Standard, which provide clear guidelines and consumer trust. The availability of certified raw materials allows brands to confidently market their products without fear of greenwashing accusations, as the audit trails are rigorous and transparent. The institutional support creates a virtuous cycle where increased demand leads to better supply security and lower relative costs over time. Furthermore, government procurement policies in several EU nations prioritize certified natural textiles for public sector uniforms, further bolstering demand. The combination of consumer trust in known labels and the logistical ease of sourcing certified natural fibers ensures that this segment remains the cornerstone of the sustainable fashion market.

The Recycled Materials segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 11.2% from 2026 to 2034 owing to the urgent need to divert textile waste from landfills, advancements in chemical recycling technologies, and the rising availability of post-consumer recycled polyester and nylon from ocean plastics. The biggest reason for the rapid expansion of the recycled materials sector is the implementation of stringent legislative mandates across the European Union that require minimum thresholds of recycled content in new textile products. Policymakers are aggressively pushing for a circular economy where waste is viewed as a resource, forcing brands to incorporate recycled fibers into their collections to comply with upcoming laws. The Extended Producer Responsibility schemes also financially incentivize the use of recycled inputs by lowering fees for companies that demonstrate high circularity rates. Furthermore, the ban on single-use plastics and the push to clean up oceans have spurred the collection of PET bottles and fishing nets, which are processed into high-quality recycled polyester and nylon for fashion. As regulatory pressure mounts, the shift from virgin to recycled materials becomes a legal necessity rather than a voluntary choice, driving unprecedented growth in this segment. Also contributing to the growth of this segment is the recent commercialization of advanced chemical recycling technologies that can break down mixed-fiber textiles and dyed fabrics into their molecular building blocks for reconstruction into virgin-quality fibers. Traditional mechanical recycling often degrades fiber quality and struggles with blends, but chemical recycling overcomes these limitations, enabling the infinite looping of materials without loss of performance. Companies are now able to recycle poly-cotton blends and colored garments into new yarns that are indistinguishable from virgin materials, opening up vast new feedstocks that were previously unrecyclable. The technological leap allows brands to claim true circularity and reduce their reliance on fossil-fuel-based virgin synthetics. The ability to process complex waste streams addresses the feedstock shortage that has historically constrained the recycled market. As these technologies mature and costs decrease, the volume of high-quality recycled materials entering the fashion supply chain will skyrocket, propelling this segment to the forefront of market growth.

By End User Insights

The Women segment held the majority share of 58.3% of the Europe sustainable fashion market in 2025 because of the historical reality that women constitute the primary purchasers of apparel and accessories, coupled with data showing that female consumers are generally more engaged with sustainability issues and ethical consumption patterns than their male counterparts. The main thing boosting the women’s segment to the top is the significantly higher frequency of clothing purchases and the diverse range of wardrobe requirements that characterize female fashion consumption. Women typically own larger wardrobes with greater variety in styles, occasions, and seasons compared to men, creating a larger volume of potential sustainable swaps. The high turnover rate provides a substantial opportunity for sustainable brands to capture market share by offering eco-friendly alternatives for every niche. The diversity of needs means that women are constantly seeking new items, and as awareness grows, they are increasingly directing this demand toward ethical brands. Furthermore, the influence of women as household purchasing managers extends beyond their own clothing to family members, amplifying their impact on the market. The sheer volume of transactions and the breadth of categories involved ensure that the women’s segment remains the financial backbone of the sustainable fashion industry, driving innovation and scale. Looking further, this segment maintains its top spot due to the stronger emotional connection female consumers tend to have with ethical values, social justice, and environmental activism, which translates into higher brand loyalty for sustainable labels. Women are often the primary drivers of social change within communities and are more likely to align their spending with their moral compass. The demographic is more active in researching brand practices, reading labels, and participating in campaigns against fast fashion exploitation. The sense of community among female shoppers, fostered through social media and word-of-mouth, accelerates the adoption of sustainable trends. When a brand proves its ethical credentials, it gains fierce advocacy from female customers who view their purchases as a vote for a better world. This deep-seated alignment between personal values and purchasing behavior creates a resilient and expanding market base that outpaces other demographics in terms of engagement and long-term commitment to sustainable fashion.

The Kids/Children segment is expected to exhibit a noteworthy CAGR of 10.5% between 2026 to 2034. This swift growth of the segment is driven by heightened parental concern over chemical exposure, the rapid physical growth of children necessitating frequent replacements, and the intergenerational transfer of environmental values. The main thing moving this segment is the intense anxiety among parents regarding the presence of harmful chemicals, allergens, and toxins in conventional clothing, given the sensitivity of young skin. Parents are increasingly scrutinizing fabric compositions and dye processes, opting for organic and non-toxic materials to protect their children’s health. The perception that sustainable equals safe is a powerful motivator, overriding price sensitivity for many families. Furthermore, the rise of “clean beauty” and non-toxic living trends has naturally extended to children’s fashion, creating a holistic lifestyle approach. As scientific evidence regarding the effects of endocrine disruptors in textiles emerges, the demand for certified safe and sustainable children’s clothing will continue to surge, making this the most dynamic growth area in the market. A further key driver for the children’s segment is the practical necessity of frequent clothing replacement due to rapid physical growth, which aligns perfectly with the principles of the circular economy and secondhand culture. Children outgrow their clothes every few months, generating a high volume of waste that parents are eager to mitigate through sustainable solutions like renting, swapping, or buying secondhand. Parents are increasingly embracing the idea that buying used or renting clothes for short periods is both economically smart and environmentally responsible. The behavioral shift reduces the barrier to entry for sustainable fashion, as the lower cost of secondhand or rented items makes ethics accessible to all income levels. The normalization of passing clothes down through siblings or friends reinforces the community aspect of sustainability. As the stigma around used clothing disappears and is replaced by a badge of ecological honor, the children’s segment benefits from a unique convergence of practical necessity and ethical idealism, fueling its status as the fastest-growing market sector.

REGIONAL ANALYSIS

Germany Sustainable Fashion Market Analysis

Germany was the top performer in the Europe sustainable fashion market and accounted for a 22.8% share in 2025. The preeminence of the German market is attributed to its deeply ingrained cultural value of “Ordnung” and environmental stewardship, which translates into high demand for certified and transparent fashion products. Besides, the nation serves as the epicenter of green consciousness on the continent, characterized by a highly informed consumer base, rigorous environmental standards, and a robust infrastructure for recycling and circular economy initiatives that set the benchmark for the rest of Europe. The discerning attitude forces retailers to maintain high standards of proof and traceability. The country’s strong legislative framework, including strict laws on supply chain due diligence, compels companies to monitor human rights and environmental impacts throughout their global value chains. Furthermore, Germany boasts one of the most advanced textile waste collection systems in Europe, facilitating high rates of reuse and recycling. The presence of major trade fairs like Premium Berlin, which focuses heavily on sustainability, reinforces the country’s role as a thought leader. The combination of regulatory pressure, consumer literacy, and infrastructural support ensures Germany remains the primary engine for sustainable fashion innovation and adoption in the region.

United Kingdom Sustainable Fashion Market Analysis

The United Kingdom followed closely behind in the European sustainable fashion market and occupied a share of 18.7% in 2025. This growth of the UK market is driven by a unique blend of grassroots activism and corporate responsiveness, fueled by a media landscape that frequently highlights environmental issues in fashion. In addition, the British market is distinguished by its vibrant scene of independent ethical designers, a strong secondhand and vintage culture, and a proactive civil society that holds major corporations accountable through campaigning and media scrutiny. The thriving circular market is supported by popular platforms and charity shops that normalize pre-loved fashion. The influence of high-profile campaigns by organizations like Fashion Revolution, which originated in the UK following the Rana Plaza disaster, keeps sustainability at the forefront of public discourse. Furthermore, the UK government’s inquiry into the sustainability of the fashion industry has led to increased scrutiny and voluntary codes of practice. The concentration of fashion education institutions focusing on sustainable design in London also feeds a pipeline of innovative talent. The synergy between an active citizenry, a dynamic resale sector, and a responsive retail industry positions the UK as a critical hub for sustainable fashion evolution.

France Sustainable Fashion Market Analysis

France plays a key role in the Europe sustainable fashion market due to groundbreaking legislation and the pivot of its prestigious luxury houses toward sustainable practices, recognizing that exclusivity now includes environmental integrity. The French market is defined by its strategic integration of sustainability into the luxury sector, strong government legislation against waste, and a growing movement to reconcile the country’s heritage of high fashion with ecological responsibility. The law has fundamentally changed inventory management strategies across the industry. French consumers are increasingly valuing quality and longevity over quantity, aligning with the “slow fashion” ethos that complements the national appreciation for craftsmanship. The government’s support for local manufacturing and eco-design grants further stimulates the sector. By leveraging its global influence in luxury, France is setting a tone that sustainability is synonymous with prestige, driving market growth through high-value segments.

Italy Sustainable Fashion Market Analysis

Italy is moving ahead steadfastly in the European sustainable fashion market owing to its position as a global hub for textile production, where manufacturers are adopting advanced technologies to reduce water and energy usage while maintaining the high quality associated with Made in Italy. The Italian market is characterized by its focus on sustainable innovation in textile manufacturing, the preservation of artisanal traditions that inherently oppose fast fashion, and a gradual but steady shift among its world-renowned fashion houses toward circularity. The tradition of producing durable, timeless pieces rather than disposable trends aligns naturally with sustainable principles, appealing to conscious consumers globally. The rise of “green” luxury brands originating from Italy is also gaining traction, combining aesthetic excellence with ethical sourcing. Furthermore, the Italian government’s incentives for Industry 4.0 technologies have enabled textile mills to implement smart monitoring systems that optimize resource efficiency. The strong export orientation of Italian fashion means that meeting international sustainability standards is a competitive necessity, driving continuous improvement. The fusion of heritage craftsmanship with modern eco-innovation ensures Italy remains a pivotal player in the high-end sustainable fashion landscape.

Sweden Sustainable Fashion Market Analysis

Sweden is anticipated to expand notably in the Europe sustainable fashion market from 2026 to 2034 due to its culture of “Lagom” or balanced living, which discourages excessive consumption and promotes mindful purchasing, alongside being the birthplace of major global initiatives like Fashion Week Stockholm’s sustainability focus. Despite its smaller population, Sweden punches above its weight as a global trendsetter in sustainability, home to pioneering circular business models, influential policy frameworks, and a consumer base that is among the most environmentally aware in the world. The country is a hotspot for innovative startups developing rental platforms, repair services, and material recycling technologies, supported by generous government grants and a supportive entrepreneurial ecosystem. The presence of global giants like H&M Group, despite controversies, has also led to massive investments in recycling research and collection schemes that influence the wider market. Swedish municipalities often lead in public procurement of sustainable uniforms and workwear, setting an example for the private sector. The combination of progressive consumer behavior, policy leadership, and a thriving startup scene makes Sweden a laboratory for sustainable fashion solutions that are eventually exported to the rest of the continent.

COMPETITIVE LANDSCAPE

The competition in the Europe sustainable fashion market is characterized by intense rivalry between established fast fashion giants agile luxury conglomerates and emerging niche brands vying for dominance through authenticity and innovation. Traditional retailers are aggressively launching eco-conscious sub-labels and circular services to prevent losing market share to digital natives who have long championed transparency as a core value proposition. The landscape is shifting from a volume-based model where speed was paramount to a value-based model where traceability and carbon footprint reduction are the new battlegrounds. Competitors are differentiating themselves through proprietary recycling technologies exclusive partnerships with material scientists and community building initiatives that foster deep brand loyalty. Greenwashing accusations have heightened scrutiny forcing companies to back claims with verified data and third-party certifications. Price wars are evident in the mass market segment while premium players compete on craftsmanship and regenerative impact. The entry of technology startups offering blockchain verification is adding a new layer of complexity forcing mid-market players to elevate their digital capabilities. Overall the market is dynamic with constant innovation in sourcing manufacturing and distribution channels as companies strive to capture the spending power of the increasingly conscious European consumer.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Plus Size Clothing Market include

- Stella McCartney

- Patagonia

- H&M Group

- Inditex (Zara)

- Adidas AG

- Puma SE

- Nike Inc.

- Levi Strauss & Co.

- Burberry Group plc

- Kering SA

- Eileen Fisher

- People Tree

- Reformation

- Armedangels

- Pangaia

Top Players in the Europe Sustainable Fashion Market

Hennes and Mauritz AB

Hennes and Mauritz AB operates as a pivotal force in the Europe sustainable fashion market through its ambitious climate positive strategy and extensive garment collecting initiatives. The company contributes globally by scaling circular business models such as repair services and resale platforms which set benchmarks for high street retailers worldwide. Recent actions to strengthen their position include the launch of Looop, an in-store recycling machine that transforms old garments into new ones without using water or chemicals. The brand has also committed to sourcing recycled or sustainably sourced materials and actively partners with innovation hubs to develop bio-based fibers. Hennes and Mauritz is integrating sustainability into its core supply chain and offering affordable eco-conscious collections. Through these actions, they continue to drive mass-market adoption of responsible fashion practices across the continent.

Kering SA

Kering SA maintains a formidable presence in the Europe sustainable fashion market by leveraging its portfolio of luxury houses to pioneer regenerative agriculture and biodiversity protection. The group contributes to the global landscape by establishing rigorous environmental profit and loss accounting standards that quantify the ecological impact of luxury production. Their recent strategic moves involve the complete elimination of virgin plastics from packaging and the implementation of strict animal welfare standards across all brands. Kering has also invested heavily in material innovation labs to develop alternative leathers and low-carbon textiles while mandating full supply chain transparency for its partners. The company recently launched a fund to support startups focused on circularity and decarbonization technologies. This commitment to embedding sustainability at the highest level of luxury solidifies their reputation as an industry leader who proves that exclusivity and environmental stewardship can coexist seamlessly.

Inditex SA

Inditex SA plays a critical role in the Europe sustainable fashion market through its Join Life collection and comprehensive roadmap to achieve net zero emissions by 2040. The Spanish giant contributes to the global ecosystem by demonstrating how fast fashion logistics can be adapted to prioritize organic cotton and recycled polyester at scale. Recent actions to bolster their market position include the introduction of made-to-order production lines that significantly reduce inventory waste and overproduction. The company has also partnered with major logistics firms to electrify its last-mile delivery fleet across European cities to lower carbon output. Inditex frequently collaborates with textile recycling innovators to close the loop on garment lifecycles and has committed to ensuring all synthetic fibers are recycled or biodegradable. Their aggressive integration of sustainability metrics into executive compensation ensures that environmental goals remain central to operational decision-making and long-term growth strategies.

Top Strategies Used by Key Market Participants

Key players in the Europe sustainable fashion market primarily employ strategies centered on circular economy integration and supply chain transparency to capture consumer loyalty. Companies are heavily investing in closed-loop systems that enable garment collection, recycling, and resale to minimize waste and extend product lifecycles. Another dominant strategy involves the adoption of digital product passports which provide consumers with detailed information regarding material origin and environmental impact. Brands are increasingly partnering with biotechnology firms to develop innovative bio-based materials that replace conventional synthetics and reduce reliance on fossil fuels. Expansion of repair and rental services is also a common tactic to address the demand for longevity and access over ownership. Furthermore, retailers are focusing on regenerative agriculture sourcing to restore ecosystems while securing raw material supplies. These approaches collectively aim to dismantle linear production models and create a resilient ethical fashion ecosystem for all.

MARKET SEGMENTATION

This research report on the Europe sustainable fashion market has been segmented and sub-segmented based on the following categories.

By Type

- Apparel

- Footwear

- Accessories

- Jewelry

By Material

- Organic/Natural Materials

- Recycled Materials

- Certified Responsible Materials

By End User

- Women

- Men

- Kids / Children

By Distribution Channel

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

{kind=link}