A recent Wall Street Journal article reignited a familiar generational feud between Millennials and Baby Boomers. Drawing on a report by AEI economist Scott Winship, the paper asked which generation had it better — and what unpacking that debate tells us about the health of our modern economy.

Predictably, Millennials and Boomers spun into a frenzy. Millennials cite soaring housing prices, student debt, and federal deficits as forces holding them back. Boomers counter by invoking 1970s stagflation, when skyrocketing inflation and sluggish growth robbed an entire generation of economic opportunity. Both make solid arguments. But in their fury to out-grieve one another, both sides miss the point.

The real question isn’t who had it worse. It’s how we can create the conditions for every generation to have it better.

The Good News Nobody Wants to Hear

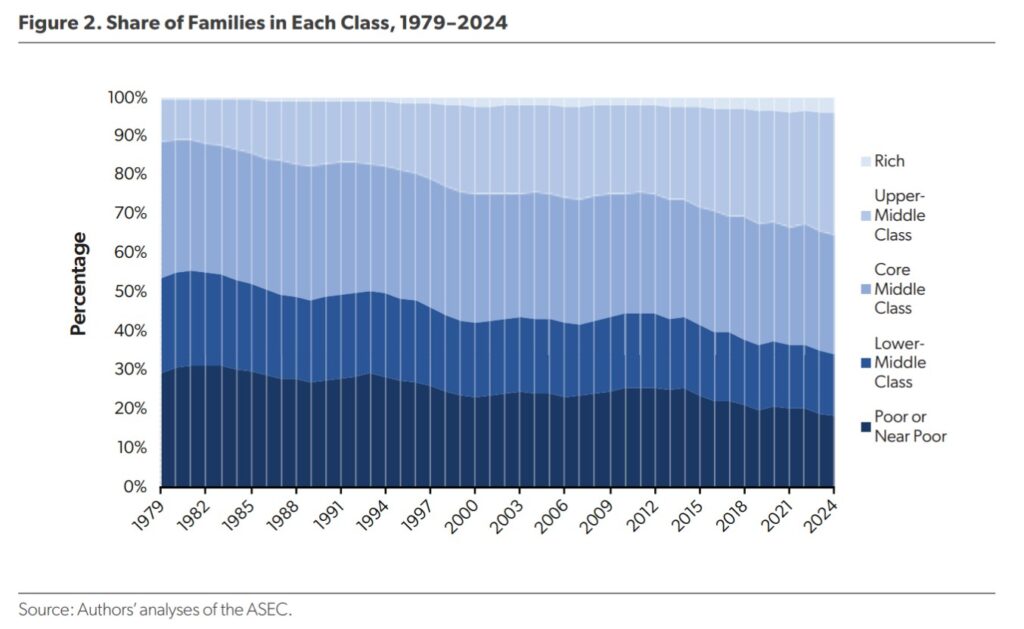

Scott Winship and his coauthor find that when you measure the middle class by purchasing power rather than by relative standing, it hasn’t hollowed out. Just the opposite. The upper-middle class expanded from 10 percent of American families in 1979 to 31 percent by 2024. The share of families too poor to reach middle-class living standards fell from 54 percent to 35 percent over the same period. Despite Millennial groans, the American middle has never been wider.

It’s not only Millennials who reap the benefits of greater economic abundance. The Economist reached a similar verdict about Gen Z, concluding that they are “unprecedentedly rich.” The typical 25-year-old Gen Zer earns an annual household income of over $40,000 — more than 50 percent above what Boomers earned at the same age, after adjusting for taxes, transfers, and inflation. Youth unemployment across the rich world recently hit the lowest point since 1991.

Even the housing and student debt objection doesn’t hold up as cleanly as advertised. In 2022, Americans under 25 spent roughly 43 percent of post-tax income on housing and education combined — slightly below the historical average for that age group from 1989 to 2019.

The Bad News Everybody Hears

Despite these gains, younger Americans face forces that older generations largely didn’t. The median home now costs more than five times the median household income, a ratio that would have seemed dystopian to the generation that bought at two or three times their salary. This explains why the age of first-time homebuyers is now edging above 40, an all-time high.

This imbalance in homeownership is deciding who gets to build wealth through the most reliable vehicle of the American Dream. Baby Boomers hold roughly half of all US wealth, or about $78 trillion, despite representing less than a quarter of the population. In an era before restrictive zoning, Boomers really did have an open door to wealth-building at an earlier age.

A Budget Mismatch

An even starker picture, though, comes from the federal balance sheet. Penn Wharton’s Budget Model recently traced the fiscal footprint of each major demographic group, including the share of federal outlays they receive. Retirees collect $2.7 trillion, or 62 cents of every dollar distributed. Working-age adults (many of them Millennials) get 28 cents. Children and young adults under 26 share 10 cents. On a per-capita basis, the gap is even more pronounced, and the retiree share is projected to only widen as the population ages.

It’s no surprise that older Americans receive an outsized portion of the federal spending pie, as they represent a large and active voting bloc. But what is puzzling is how many in this older demographic assert generational disadvantage, even as they collect a disproportionate share of federal benefits, mostly driven by Social Security and Medicare.

A Pointless Debate?

The generational debate tends to collapse into zero-sum thinking, as if the only remedy is to take from one age group and give to another. That thinking isn’t only unproductive. It’s wrong.

As I’ve argued before, the constraints squeezing younger generations are mostly self-inflicted policy failures, not the inevitable fate of demographic transition. Restrictive zoning and broken permitting systems limit housing supply precisely when young people face their sharpest cost-of-living pressures.

Worse still, the economic damage wrought by uncontrolled federal spending will fall on all generations. U.S. public debt recently crossed 100 percent of GDP for the first time since World War II. Unlike in 1946, there’s no demographic tailwind or peacetime dividend to grow our way out. Penn Wharton projects debt exceeding 190 percent of GDP by 2050. At that point, the generational debate will be long forgotten — replaced by the shared burden of a fiscal reckoning that will impact us all.

Instead of training their sights on each other, Boomers and Millennials — all generations, for that matter — should champion market-based policies that expand opportunity for everyone. Winship’s data put things in a useful perspective: even Americans at the bottom of the income distribution ended up 55 percent richer than their forebears, despite ranking lower in relative terms.

That’s the story worth telling, and one we must continue writing.

")

{kind=link}