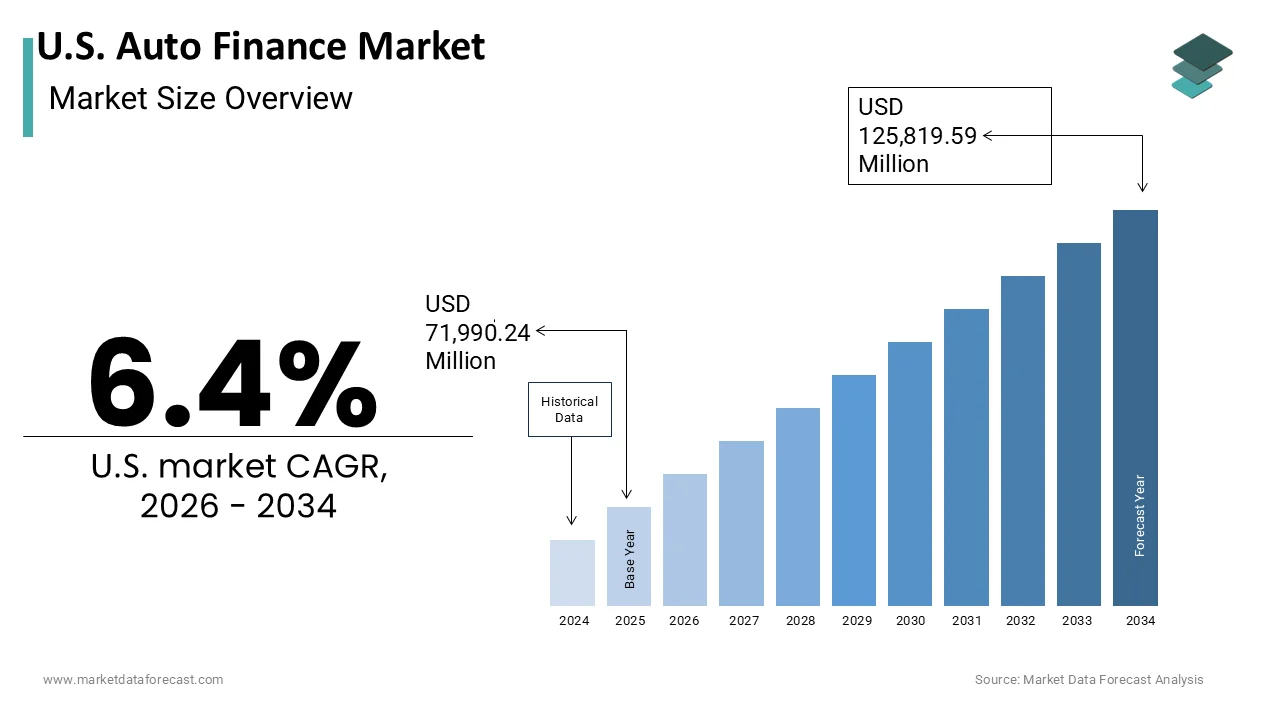

U.S. Auto Finance Market Size

The U.S. Auto Finance Market is projected to grow from USD 71,990.24 million in 2025 to USD 76,597.62 million in 2026 and reach USD 125,819.59 million by 2034, registering a CAGR of 6.4% during the forecast period from 2026 to 2034.

The U.S. auto finance market operates at the intersection of automotive retail credit risk management and consumer financial behavior and is deeply integrated into the broader U.S. credit system. According to the Federal Reserve Bank of New York, total outstanding auto loan debt in the U.S. reached 1.607 trillion U.S. dollars in the fourth quarter of 2023, reflecting its significance in household balance sheets. As per the Bureau of Consumer Financial Protection, approximately 86% of new vehicle purchases and 55% of used vehicle transactions involve some form of financing. The sector is governed by a combination of federal regulations, including the Truth in Lending Act, and state-level usury laws that cap interest rates and mandate disclosure standards. Unlike unsecured lending, auto finance is asset-backed, which influences risk pricing and recovery mechanisms. The market’s health is closely tied to macroeconomic conditions, including interest rates, unemployment levels, and vehicle depreciation trends, making it a sensitive barometer of both consumer confidence and automotive industry dynamics.

MARKET DRIVERS

High Reliance on Vehicle Ownership for Daily Mobility Sustains Persistent Financing Demand

Automobile dependency remains deeply entrenched in American life due to limited public transit infrastructure and dispersed urban planning, which is a key factor propelling the U.S. auto finance market growth. As per the Federal Highway Administration, the average American driver drives 13,476 miles per year. In rural and suburban areas where public transportation is minimal or nonexistent, non-vehicle access is essential for employment, ent education, and healthcare. According to the Brookings Institution, over 40% of zero vehicle commuters in 77 of the 100 largest metropolitan areas drive to work. This structural necessity translates into consistent demand for vehicle acquisition even during economic downturns. As per the Bureau of Consumer Financial Protection, more than 90% of American households have a vehicle, underscoring near universal adoption. Consequently, financing becomes a practical necessity for the majority of buyers,s given that the average new vehicle price exceeded 48,000 U.S. dollars in 20,23 according to Kelley Blue Book. This socioeconomic reality ensures a steady pipeline of credit seekers regardless of short-term market fluctuations.

Integration of Digital Retail and Embedded Finance Transforms Consumer Acquisition Pathways

The digitization of car buying has fundamentally reshaped how consumers access and secure auto financing, which is further boosting the U.S. market expansion. According to Cox Automotive, over 78% of new vehicle shoppers in 2023 began their journey online,e with 62% expressing willingness to complete the entire purchase,se including financing, ing digitally. Automakers and dealers have responded by embedding pre-approval tools directly into their websites and mobile apps, enabling real-time credit decisions. Captive lenders like Ford Credit and GM Financial now offer soft credit pulls that generate personalized rate quotes within seconds without impacting credit scores. The Federal Reserve’s 2023 Survey of Consumer Finances noted that 41% of auto loans originated through digital channels, up from 24% in 2019. Additionally,y fintech partnerships such as Carvana’s integration with Credit Acceptance and CarMax’s alliance with Santander Consumer USA streamline loan disbursement and title processing. This seamless convergence of e-commerce and credit reduces friction, increases conversion rate,s and expands access to financing for tech-savvy consumers who expect Amazon-like purchasing experiences in automotive retail.

MARKET RESTRAINTS

Elevated Interest Rates Increase Borrowing Costs and Constrain Affordability

The Federal Reserve’s aggressive monetary tightening cycle has significantly raised the cost of auto financing across risk tiers, which is one of the major factors hampering the growth of the U.S. auto insurance market. As per the Federal Reserve Bank of St Louis, the average interest rate on a 60-month new car loan rose from 4.52% in early 2022 to 7.82% by December 2023. For subprime borrowers with credit scores below 600, rates frequently exceed 18% according to data from Experian’s State of the Automotive Finance Market. These elevated rates directly impact monthly payments with a typical 48,000 U.S. dollar vehicle now costing over 950 U.S. dollars per month,h including interest, st compared to 720 U.S. dollars in 2021. The Bureau of Labor Statistics reports that transportation accounts for 16.8% of average household expenditure, res making it the second largest budget category after housing. Higher payments force consumers to extend loan terms, with 43% of new auto loans in 2023 exceeding 72 months, as documented by the Federal Reserve Bank of New York. This affordability squeeze reduces demand, particularly for price-sensitive buyers, and increases default risk as debt service burdens rise.

Rising Delinquency Rates Signal Deteriorating Credit Quality in Subprime Segments

Deteriorating repayment performance, particularly among high-risk borrowers, is emerging as a systemic concern for lenders, which is further impeding the U.S. auto insurance market expansion. According to the Federal Reserve Bank of New York, the annualized transition rate of auto loans into delinquency reached 7.7% in the fourth quarter of 2023. Subprime accounts,s which represent 22% of all autooriginationso, ns accounted for 68% of all delinquencies as per S and P Global Mobility’s 2023 Auto Finance Report. The Consumer Financial Protection Bureau identified in its 2023 supervisory highlights that lenders offering loans with terms exceeding 84 months saw delinquency rates 2.3 times higher than standard 60-month contracts. Contributing factors include vehicle depreciation outpacing loan paydown, negative equity rollover, and inflation-driven pressure on disposable income. As unemployment remains low but wage growth lags behind price increases, many borrowers face cash flow strain. These credit deterioration forces lenders to tighten underwriting standards, reduce exposure to deep subprime segments, ts and increase a loss reserve,rve which in turn restricts credit availability for marginal borrowers and dampens overall market volume.

MARKET OPPORTUNITIES

Expansion of Specialized Lending for Electric Vehicles Creates Niche Growth Corridors

Automakers and financial institutions are developing tailored financing products to accelerate electric vehicle adoption, which is a promising opportunity for the U.S. auto insurance market. According to the Department of Energy, more than 1.2 million EVs were sold in the U.S. in 2023, representing 7.6% oflight-dutyht duty sales. Recognizing higher upfront costs, lenders are introducing incentives such as below-market interest rates, extended terms,s and bundled charging credits. Ford Credit offers 2.9% APR for 72 months on Mustang Mach-E purchases, while GM Financial provides 1,000 U.S. dollars toward home charger installation with EV leases. The Inflation Reduction Act’s 4,000 U.S. dollar used EV and 7,500 U.S. dollar new EV tax credits are increasingly being monetized at the point of sale through lender partnerships, enabling immediate price reductions. As per J D Powe,r 68% of EV buyers in 2023 utilized manufacturer-sponsored financing compared to 52% for internal combustion vehicles. Additionally, credit unions like Alliant and PenFed have launched green auto loan programs with rate discounts for zero-emission vehicles. These targeted financial instruments lower effective acquisition costs and address range and charging anxiety by integrating mobility services into the financing package.

Growth of Subscription and Flexible Ownership Models Opens Alternative Revenue Streams

Beyond traditional loans and leases, the U.S. auto finance market is embracing flexible mobility solutions that blend financing, insurance,e and maintenance into a single monthly payment. According to McKinsey and Company, over 1.1 million Americans subscribed to vehicle programs in 2023, with offerings from automakers like Care by Volvo and third parties like Fair and Autonomy. These models appeal to urban professionals and gig economy workers who seek short-term commitments without long-term depreciation risk. Captive lenders are structuring these products as operating leases with embedded residual value guarantees and dynamic pricing based on mileage and duration. The Federal Reserve’s 2023 Financial Stability Report noted that securitization of subscription receivables is emerging as a new asset class attracting institutional investors. Additionally, these programs generate rich usage data that informs credit scoring for in-file consumers. As consumer preferences shift toward access over ownership, finance providers are repositioning from transactional lenders to mobility service enablers, creating recurring revenue and deeper customer engagement.

MARKET CHALLENGES

Regulatory Scrutiny on Discriminatory Lending Practices Intensifies Compliance Burdens

Federal and state regulators are intensifying oversight of auto lending to address disparities in pricing and access, which is a significant challenge to the U.S. auto insurance market expansion. According to the Consumer Financial Protection Bureau, its 2023 enforcement actions included three major consent orders against auto lenders for alleged markups that disproportionately affected minority borrowers. The Department of Justice’s Fair Lending Initiative has reopened investigations into dealer reserve policies where finance managers add discretionary rate markups. In California,nia the Department of Financial Protection and Innovation implemented a 2023 rule requiring lenders to provide level demographic data, including race and ethnicity inferred from applicant names and addresses. These measures increase operational complexity as lenders must implement algorithmic fairness audits and revise compensation structures. Non-compliance risks fines,s reputational damage,ge and loss of dealer network partnerships. As per the American Bankers Association, ion 74% of auto lenders increased compliance staffing in 2023 to navigate evolving fair lending expectations, creating cost pressures that may reduce risk appetite for non-prime segments.

Vehicle Depreciation Volatility Complicates Residual Value Estimation and Lease Risk Management

Unpredictable shifts in used car values pose significant challenges to the expansion of the U.S. auto finance market. According to Black Book, the average three-year-old vehicle retained 58% of its original value in 2023, down from 68% in 202,1 due to post-pandemic inventory normalization. This 10 percentage point decline translates to thousands of dollars in unexpected losses per leased vehicle for captive finance companies. The volatility stems from supply chain disruptions, semiconductor shortages,s and fluctuating consumer preferences, particularly around electric vehicles,s whose resale values remain uncertain. As per A, LG residual value forecasts for EVs vary by as much as 15 percentage points between models due to charging infrastructure gaps and battery degradation concerns. Lenders must now employ dynamic pricing models that incorporate real-time auction data and macroeconomic indicators to adjust lease terms monthly. This complexity increases capital requirements and reduces profitability, particularly for long-term leases. Consequently, many lenders are shortening lease durations or shifting toward closed-end loans to mitigate residual risk in an increasingly unpredictable asset market.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Provider Type, Purpose Type, Vehicle Type, and Region. |

|

Various Analyses Covered |

Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

California, Texas, Florida, New York, and the rest of the United States |

|

Market Leaders Profiled |

Ally Financial Inc., Capital One Financial Corporation, Ford Motor Credit Company LLC, Toyota Financial Services, GM Financial Inc., Wells Fargo & Company, Bank of America Corporation, JPMorgan Chase & Co., Santander Consumer USA Holdings Inc., TD Auto Finance, Huntington Bancshares Incorporated, Credit Acceptance Corporation |

SEGMENTAL ANALYSIS

By Provider Type Insights

The OEM segment held the major share of the U.S. auto finance market in 2025 and is likely to experience high captive program integration and optimized dealer networks for the next few years. This dominance stems from their strategic alignment with manufacturer sales objectives and ability to offer highly tailored financial incentives. According to the Federal Reserve Bank of New York, OEM captives financed 68% of all new light-duty vehicle sales in 2023, leveraging below-market interest rates, cash rebates, and lease loyalty programs to drive volume. Companies like Ford Credit, GM Financial,l and Toyota Financial Services embed financing offers directly into dealership point of sales systems, enabling instant approvals and seamless transaction closure. The National Automobile Dealers Association reports that 74% of franchised dealers prioritize OEM financing due to streamlined processing and higher approval rates for marginal credit profiles. Additionally, captives benefit from superior residual value forecasting for leasing,g which reduces risk and enhances profitability. Their integrated position within the automotive value chain allows them to respond rapidly to inventory shifts and consumer demand signals,l s making them indispensable partners in modern vehicle retail.

The other segment is estimated to record the fastest CAGR in the U.S. market during the forecast period, owing to the rising consumer demand for frictionless digital experiences and gaps in traditional underwriting for non-prime borrowers. According to the Consumer Financial Protection Bureau, approximately 26 million U.S. adults are considered credit invisible, yet require vehicle access for employment. J D Power’s 2023 U.S. Auto Finance Satisfaction Study found that digital lenders scored 22 points higher in application ease than traditional banks. The Federal Reserve’s 2023 Survey of Household Economics noted that 58% of subprime borrowers now initiate financing online before visiting a dealership. Additionally, our partnerships with buy here, pay here dealers and online retailers enable fintechs to reach underserved segments excluded from mainstream channels. These capabilities position digital lenders as critical enablers of financial inclusion and e-commerce integration in the evolving auto finance landscape.

By Purpose Type Insights

The loan segment led the market by capturing the largest share of the U.S. auto finance market in 2025. This predominance is driven by the structure of the used vehicle market, where leasing is virtually nonexistent,t and by economic uncertainty that favors asset retention. According to Experian’s State of the Automotive Finance Market, 89% of used vehicle transactions in 2023 were financed through loans compared to only 11% for leases. The average loan term has extended to 72 months for new vehicles and 68 months for used units,s enabling lower monthly payments amid high vehicle prices. According to the Federal Reserve Board, over 60% of vehicle owners report using their vehicle to commute to work or school, justifying ownership. Additionally, ly rising interest rates have made lease residuals harder to predict, thus reducing manufacturer enthusiasm for leasing programs. This cultural and economic alignment ensures loans remain the default financing mechanism across income and credit spectrums.

The leasing segment is estimated to register a promising CAGR in the U.S. market during the forecast period due to the resurgence of electric vehicles and corporate fleet modernization. According to Cox Automo,tive EVs represented 38% of all leased vehicles in 202, despite accounting for only 7.6% of total sales, indicating strong consumer preferenshort-termrt term EV commitments due to battery and technology obsolescence concerns. Automakers are actively promoting leasing through subsidized residuals and maintenance bundles, with Tesla, BMW B,, and Hyundai offering all-inclusive lease packages. The Bureau of Economic Analysis reports that corporate fleet leasing grew by 12% in 2023 as businesses seek to manage balance sheet exposure and comply with ESG mandates. Additionally, the Inflation Reduction Act’s tax credit rules favor leasing by allowing the full 7,500 U.S. dollar credit to be passed through to lessees immediately. These structural advantages position leasing as a strategic tool for technology adoption and fleet turnover in an era of rapid automotive innovation.

By Vehicle Type Insights

The passenger car segment accounted for the largest share of the U.S. auto finance market in 2025 and is likely to retain its primary volume position and drive substantial retail credit demand for the next few years. This segment includes sedans, SUVs, and crossovers used primarily for personal and household transportation. As per the Bureau of Consumer Financial Protection, more than 90% of American households have a vehicle, with SUVs and trucks accounting for 78% of new retail sales in 2,023 according to National Automobile Dealers Association data. Financing demand is amplified by high transaction prices, with the average financed new passenger vehicle amounting to 42,300 U.S. dollars as per the Federal Reserve Bank of New York. Captive lenders and banks have optimized underwriting models for this segment,gment offering tiered rates based on credit score lo, a loan term, and down payment. Additionallyi,tionally digital retail platforms prioritize passenger vehicle financing due to higher transaction volumes and standardized valuation. The cultural centrality of personal vehicle ownership in American life ensures sustained and predictable demand for consumer auto loans and leases.

The commercial vehicles segment is anticipated to record a CAGR of 12.2% during the forecast period in the U., S. marketng to the e-commerce logistics and small business formation. According to the U.S. Census Bureau, over 5.4 million new business applications were filed in 2023, many requiring delivery vans or service trucks for operations. The National Retail Federation reports that 22 billion parcels were delivered in the U.S. in 202,3 necessitating over 150,000 new light commercial vehicles financed primarily through business loans. Lenders like Bank of America and Wells Fargo have launched dedicated small business auto finance portals offering higher loan limits and longer terms for commercial chassis. Additionally, ly the rise of gig economy platforms such as Uber Freight and DoorDash has spurred independent contractor vehicle acquisition, often financed through specialized programs from lenders like Santander. The Bureau of Labor Statistics notes that transportation and warehousing employment grew by 4.7% in 202,3 further expanding the commercial vehicle financing base. This convergence of entrepreneurs, IP logistics,ics, and platform work is transforming commercial auto finance in the high-growth corridor.

COMPETITIVE LANDSCAPE

Competition in the U.S. auto finance market is intense and multifaceted, involving banks, credit unions, ns captive finance companies, and digital lenders vying for share across new, used, a nd commercial vehicle segments. Captive lenders such as Toyota Financial Services and Ford Credit leverage manufacturer alignment to offer subsidized rates and seamless integration with sales incentives,ntives giving them an edge in new vehicle financing. Banks like Wells Fargo and JPMorgan Chase compete on brand cross-selling opportunities and robust digital platforms,s while credit unions emphasize member-focused rates and community lending. Digital disruptors, including Carvana and Credit Acceptance,e target underserved credit segments with alternative underwriting and fully online experiences. The competitive landscape is further shaped by macroeconomic headwinds, ds including elevated interest rates,tes which compress margins and increase delinquency risks. Lenders are responding by tightening underwriting, ting extending loan terms, and diversifying into leasing and subscription models. Regulatory scrutiny on fair lending and fee transparency adds compliance complexity. Success increasingly depends on the ability to balance-adjust returns with customer experience innovation and operational agility in a market where financing is no longer a back-office function but a core component of automotive retail strategy.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. Auto Finance Market include

- Ally Financial Inc.

- Capital One Financial Corporation

- Ford Motor Credit Company LLC

- Toyota Financial Services

- GM Financial Inc.

- Wells Fargo & Company

- Bank of America Corporation

- JPMorgan Chase & Co.

- Santander Consumer USA Holdings Inc.

- TD Auto Finance

- Huntington Bancshares Incorporated

- Credit Acceptance Corporation

TOP LEADING PLAYERS IN THE MARKET

- Ally Financial Inc is a leading digital financial services company with a dominant presence in the U.S. auto finance sector. The company provides retail and wholesale financing for new and used vehicles through a nationwide network of franchised dealerships. Ally leverages advanced data analytics and a fully digital origination platform to deliver rapid credit decisions and personalized loan terms. In recent years, the company has expanded its used vehicle financing programs and introduced flexible payment options to address affordability challenges. Ally also enhanced its dealer portal with real-time inventory financing tools and integrated F&I product offerings. These initiatives reinforce Ally’s position as a technology-driven lender that prioritizes seamless dealer collaboration and consumer-centric innovation in an increasingly digital automotive retail environment.

- Wells Fargo Auto is a major division of Wells Fargo Bank offering comprehensive auto lending solutions across the U.S. The company finances both new and used vehicle purchases for consumers and provides floorplan financing to dealerships. Wells Fargo has strengthened its market position by integrating auto loan applications into its broader digital banking ecosystem, enabling existing customers to access pre-approved offers instantly. The bank also launched a suite of financial wellness tools that help borrowers manage payments and avoid delinquency. In response to evolving credit conditions,s WellsFargo refinedd irisk-basededd pricing models and expanded its near-prime lending criteria. These strategic enhancements allow the bank to maintain disciplined underwriting while serving a diverse customer base across multiple credit tiers.

- Toyota Financial Services is the captive finance arm of Toyota Motor North America and a key enabler of the brand’s U.S. sales strategy. The company offers retail loans, leases,s and commercial fleet financing tailored to Toyota and Lexus customers. Known for competitive rates and high approval rates, Toyota Financial Services integrates financing offers directly into dealership workflows and the automaker’s digital retail platforms. Recently,tly the company introduced special financing programs for electric and hybrid vehicles, including below-market interest rates and bundled charging credits. It also expanded its online lease return and equity trade-in tools to improve customer retention. These actions underscore its role not only as a lender but as a strategic partner in enhancing the end-to-end ownership experience and supporting Toyota’s electrification roadmap.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the U.S. auto finance market employ a range of strategic initiatives to navigate rising interest rates, evolving consumer expectations,s and regulatory pressures. Digital transformation iscentra ll with lenders investing in end-to-end online origination platforms that deliver instant pre-approvals and e-signing capabilities. Risk segmentation has become more sophisticated as lenders use alternative data and machine learning to serve near-prime and thin-file borrowers while maintaining portfolio quality. Strategic partnerships with dealers and digital retailers enable embedded finance experiences that reduce friction and increase conversion. Captive lenders align financing incentives with vehicle inventory and marketing campaigns to drive sales velocity. Additionally, institutions are enhancing borrower support through payment flexibility programs, financial education tools,s and early delinquency intervention systems to mitigate credit risk in high-rate environments.

MARKET SEGMENTATION

This research report on the U.S. auto finance market is segmented and sub-segmented into the following categories.

By Provider Type

- OEMs (Captive Finance Companies)

- Banks

- Credit Unions

- Fintech Lenders

- Others

By Purpose Type

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

By Country

- California

- Texas

- Florida

- New York

- Rest of the United States

{kind=link}